Regularization

When we use regression models to train

some data, there is a good chance that the model will overfit the given

training data set. Regularization helps sort this overfitting problem by

restricting the degrees of freedom of a given equation i.e. simply reducing the

number of degrees of a polynomial function by reducing their corresponding

weights.

In a linear equation, we do not want huge weights/coefficients as a small

change in weight can make a large difference for the dependent variable (Y).

So, regularization constraints the weights of such features to avoid

overfitting.

To get the best fit line, we

try to minimize the cost function given as:

To regularize the

model, a Shrinkage penalty is added to the cost function.

Types of Regularization:-

LASSO(Least Absolute Shrinkage and Selection

Operator) Regression (L1 Form)

LASSO regression penalizes the model based on the sum

of the magnitude of the coefficients. The regularization term is given by

regularization=

Where λ is the shrinkage factor.

and hence the formula for loss after regularization

is:

Ridge Regression (L2 Form)

Ridge regression penalizes the model based on the sum

of squares of the magnitude of the coefficients. The regularization term is given

by

regularization=

Where λ is the shrinkage factor.

and hence the formula for loss after regularization

is:

This value of lambda

can be anything and should be calculated by cross-validation as to what suits

the model.

Difference

between Ridge and Lasso

Ridge regression

shrinks the coefficients for those predictors which contribute very little in the

model but have huge weights, very close to zero. But it never makes them

exactly zero. Thus, the final model will still contain all those predictors,

though with fewer weights. This doesn’t help in interpreting the model very

well. This is where Lasso regression differs from Ridge regression. In Lasso,

the L1 penalty does reduce some coefficients exactly to zero when we use a

sufficiently large tuning parameter λ. So, in addition to regularizing, lasso

also performs feature selection.

Why use

Regularization?

Regularization helps

to reduce the variance of the model, without a substantial increase in the

bias. If there is variance in the model that means that the model won’t fit

well for a dataset different than training data. The tuning parameter λ controls

this bias and variance tradeoff. When the value of λ is increased up to a

certain limit, it reduces the variance without losing any important properties

in the data. But after a certain limit, the model will start losing some

important properties which will increase the bias in the data. Thus, the selection

of the good value of λ is the key. The value of λ is selected using

cross-validation methods. A set of λ is selected and cross-validation error is

calculated for each value of λ and that value of λ is selected for which the

cross-validation error is minimum.

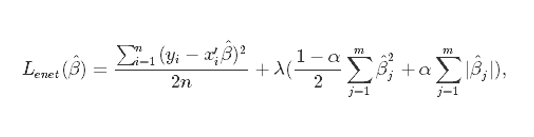

Elastic Net

According to the

Hands-on Machine Learning book, elastic Net is a middle ground between Ridge

Regression and Lasso Regression. The regularization term is a simple mix of

both Ridge and Lasso’s regularization terms, and you can control the mix ratio

α.

where α is the mixing

parameter between ridge (α = 0) and lasso (α = 1).

When should you use plain Linear? Regression (i.e., without any regularization), Ridge, Lasso, or Elastic Net?

According to the Hands-on Machine Learning book, it is

almost always preferable to have at least a little bit of regularization, so

generally, you should avoid plain Linear Regression. Ridge is a good default,

but if you suspect that only a few features are actually useful, you should

prefer Lasso or Elastic Net since they tend to reduce the useless features’

weights down to zero as we have discussed. In general, Elastic Net is preferred

over Lasso since Lasso may behave erratically when the number of features is

greater than the number of training instances or when several features are

strongly correlated.

0 Comments